Are subsidies provided to farmers in the EU generating deforestation in Brazil? Or the decline of pastoral communities in Sahel? In this article, we shed light on the CAP’s implications beyond the EU, focusing on its influence on the global trade of soya and milk products and examining its implications for local populations.

By Laurent Levard, program officer for agricultural development at Gret

Introduction

The Common Agricultural Policy (CAP) is a policy of the European Union that mainly focuses on agriculture and the food system in each Member State. However, the CAP also has a decisive influence on the European Union’s external trade (imports and exports). It therefore has an impact on agriculture and farming in the countries with which it trades.

The impact of the CAP on peasant farming in developing countries is mostly indirect: the CAP largely influences the European agricultural and food system, which in turn often has a negative impact on peasant farming in developing countries.

Moreover, the CAP is not the only policy in the equation. Other policies implemented by the European Union or its Member States also have external impacts, in particular trade, energy, environmental, food, transport, competition law and cooperation policies. In reality, it is the combination of the CAP and other European and national policies that determines the development of the European agricultural and food system and has a negative impact on farmers in the South.

In this article, we will look successively at two examples of the impact of the CAP on farmers in the South: firstly, the role of the CAP in soya imports and the impact of these imports on producer countries in Latin America, and secondly, its effects on exports of milk and milk-derived products and the impact of these exports on importing countries in Africa.

European imports of South American soya

Every year, the EU imports almost 40 million tonnes of soya (soya meal equivalent), either in the form of grain or meal. These imports, intended for animal feed, mainly provide a protein supplement to the feed ration. The maize-soya combination has formed the basis for the development of intensive livestock farming in Europe, both for cattle, where maize is consumed in the form of silage, and for pigs and poultry, where maize is consumed in the form of grain.

Between the 1960s and the end of the 2000s, European imports of soya increased thirteen-fold. After peaking in 2007, these imports have fallen back slightly due to the slower growth in livestock farming (lower meat consumption) and increased consumption of rapeseed meal, which is replacing soya. European soya imports come mainly from South America. In the various countries concerned (mainly Brazil, but also Argentina, Paraguay, Uruguay and Bolivia), the expansion of soya monocultures, mainly GMOs, has been meteoric since the 1990s.

Today, global demand for soya and the expansion of its cultivation in South America are mainly driven by China and other emerging countries. The European Union’s relative share of world imports is much smaller than it was twenty years ago, but remains significant (around 20%).

The expansion of soya cultivation in South America is largely responsible for the continent’s massive deforestation (Amazonia, Brazilian Cerrado, etc.), the loss of biodiversity, environmental contamination and the poisoning of populations through the intensive use of pesticides. Massive deforestation is also a key cause of global climate change.

The impacts of the soya model are far from being confined to farmers, but the peasant populations of the countries concerned are the main victims. They are also tending to be expropriated from their land and their livelihoods for the benefit of agribusiness firms.

Admittedly, in certain regions of Brazil and Argentina, soya cultivation has also developed within family farming, which has benefited from a genuine economic dynamism. However, these benefits are fragile, as farmers have lost all autonomy, health problems linked to the growing use of pesticides are constantly on the increase. In some regions, specialisation in soya has weakened the least competitive peasant farms, which end up having to give up their land to large farms.

The role of CAP

The decision to direct most of the CAP budget towards decoupled direct payments (independent of the type of crop) on the basis of surface area, subject to very few environmental requirements, has stimulated input-intensive agricultural production (fertilisers, pesticides, irrigation water) of high-energy concentrated fodder (cereals, silage maize) and reduced their cost price.

The availability of low-cost soya – due to productivity conditions in producer countries and the absence of customs duties – has encouraged the use of these energy fodders. Soya, which is very rich in protein, combines perfectly with energy-rich concentrated feeds. This development has therefore been to the detriment of grassland systems which based on the use of fodder that is less concentrated in energy and protein.

The rare coupled aids – designed and calculated according to specific objectives – and the various aids under the second pillar of the CAP (the part of the CAP devoted to rural development) are insufficient to significantly offset the decoupled aids under the first pillar and enable the EU to massively substitute South American soya with locally-sourced plant proteins.

It should be pointed out that coupled payments can apply to the production of plant proteins and thus stimulate EU production. Over the last three years, plant protein[1] coupled aid has been used by 19 Member States, accounting for 1.3% of total direct aid for all Member States (i.e. €473 million).

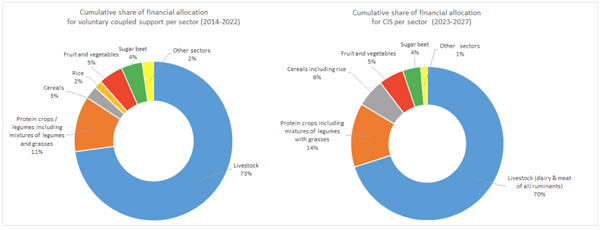

Overall, the new CAP maintains the existing system of coupled aid, with a ceiling of 13% of direct aid under the first pillar for all coupled aid, plus 2% if a Member State decides to increase the amount earmarked specifically for plant proteins. In the end, for the 2023-2027 programming, 7% of the CAP budget has been allocated to coupled payments, amonst which only 14% is dedicated to protein crops.

The amount allocated by the Member States to plant proteins therefore remains relatively low if you compare it to the 70% of coupled payment budget allocated to livestock support. Moreover, when comparing this CAP programming with the previous one, it is clear that the overall distribution of budget remains largely unchanged.

It should also be noted that the introduction of eco-regimes under the new CAP could result in incentives to develop the cultivation of plant proteins, for example through measures to promote crop diversification in crop rotations.

Milk and Milk-Derived Product Exports in Africa

The European Union exports various agricultural raw materials (cereals, dairy products, etc.) at low prices, particularly to countries in the South where these products compete with products from local agriculture. This is particularly true of exports of milk powder to the West African region and, even more so, of exports of fat-filled milk powders (FFMP).

Against a backdrop of strong demand for butter on the world market, more and more players in the dairy industry are tending to skim milk and replace animal fat most often with palm oil fat, the price of which is six to ten times lower than that of butter. After dehydration, the resulting milkfat powder is sold in developing countries at an average price 30% lower than whole milk powder.

While there were relatively few imports of FFMP some fifteen years ago, West African imports have recently soared to the point where they now account for the vast majority of the volumes of dairy powders imported by the region.

West African imports of milk and milk-derived products help to make up for the shortfall in regional production (which only covers around 40% of consumption) and, since the development of milk powders, to lower the cost to consumers.

The problem is that, because of this low price, dairy processors have a strong interest in importing powder and processing it into liquid milk or yoghurts, rather than sourcing locally from farmers. Consumers with low purchasing power also prefer imported powder and the products made from it because of their attractive price. Eventually, eating habits will change and the younger urban generations will prefer the taste of products made from imported powders to those made from local milk.

At a time when the local milk sector is facing a number of difficulties (insufficient fodder production, high seasonal fluctuations, poor development of collection and processing networks), an additional factor is hampering its development: low-price competition from milk powders.

Given the importance of livestock farming in terms of job creation, income and food security in the Sahel regions, which are currently experiencing major conflicts, it is easy to understand the extent of the damage caused by this competition. What’s more, at the other end of the FFMP chain, it is the Asian forests that are being sacrificed for the development of palm cultivation.

The role of CAP

Here too, the CAP is far from being solely responsible for the situation. The political choices made by West African countries not to protect their livestock farmers against competition from low-cost imports are part of the problem. Customs duties in the West African region on imported powder are just 5%, compared with 60% for the countries of the East African Community, for example. And let’s not the pressure exerted by the European Union on African countries to further liberalise their markets under the Economic Partnership Agreements (EPAs).

However, the CAP also has its share of responsibility: by abandoning any policy of controlling production volumes following the abolition of milk quotas in 2016, the EU Member States have encouraged the production of milk surpluses.

What’s more, the system of decoupled direct payments means that a significant proportion of farmers’ agricultural income is obtained not from the sale of their products but from these European subsidies. In reality, these direct payments do not help to improve farmers’ incomes, but enable manufacturers to pay a lower price for milk and therefore to sell their production (particularly milk powder) at a more competitive price on the world market.

While the existence of subsidies for European farmers may be perfectly legitimate, the problem is that this system is ultimately used for dumping practices, i.e. selling products at a price below their true production cost. The agricultural economist Jacques Berthelot has calculated that the dumping rate for dairy exports to West Africa, i.e. the gain in competitiveness linked to direct CAP aid, amounted to 21% of the price of the products.

Conclusion

Given the involvement of these different policies, it is not possible to quantify the extent to which each of them is responsible for the negative impact of European policies on farmers in developing countries. However, as we have seen with two examples, it is possible to clearly identify the specific tools of the CAP that influence the transformation of agriculture and thus contribute to these impacts.

These include, in particular, the mechanism of direct payments under the first ‘pillar’ of the CAP, which are decoupled and therefore not linked to clearly identified objectives, and, moreover, accompanied by a lack of strong conditionalities and reimbursement mechanisms when products are being exported to the world market.

In addition, the mechanisms for regulating agricultural markets, which made it possible to limit surpluses and maintain prices at a certain level, particularly in the case of milk with milk quotas, have been abandoned. However, market regulation has not been completely abandoned, and this practice has even been strengthened under the 2023-2027 CAP as part of the regulations relating to the Common Market Organisation (CMO). Support can be provided for voluntary production cuts in the event of a crisis.

However, this ‘safety net’ mechanism only comes into play in exceptional cases and does not compensate for the permanent dumping effect described above. This change in market regulation tends to accentuate the EU’s capacity to export agricultural products at low prices to the markets of southern countries.

[1] plant proteins: – seed legumes, dehydrated fodder legumes or legumes for seed production. – fodder legumes (in lowland and piedmont areas / in mountain areas).

Download this article as a PDF

This article is produced in cooperation with the

This article is produced in cooperation with the

Heinrich Böll Stiftung European Union.

More on CAP Strategic Plans

French CAP Strategic Plan : EU Sued over Approval of the Plan

“A Fairer CAP”, Really? | Analysing Fairwashing in CAP Talks and Practices

CAP Environmental Derogations: What is the Impact on Food Security?

CAP post-2027: An Integrated Rural and Agricultural Policy – Part 2

CAP post-2027: An Integrated Rural and Agricultural Policy – Part 1

Can the CAP Strategic Plans Help in Reaching our Pesticide Reduction Goals?

Wallonia’s Observation Letter: A plan that fails to address climate and biodiversity crises

CAP Strategic Plans and Food Security: Fallow Lands, Feeds, and Transitioning the Livestock Industry

A Just and Green CAP and Trade Policy in and Beyond the EU – Part 2

A Just and Green CAP and Trade Policy in and Beyond the EU: Part 1

Bulgaria’s CAP Strategic Plan: Backsliding on Nature and Biodiversity

Changes “required” to Ireland’s CAP Strategic Plan – European Commission

French CAP Plan: What Opportunities for Change During the New 2022-27 Presidential Term?

CAP, Fairness and the Merits of a Unique Beneficiary Code – Matteo Metta on Ireland’s Draft Plan

ARC Launches New Report on CAP as Member States Submit Strategic Plans

Slashing Space for Nature? Ireland Backsliding on CAP basics

Quality Schemes – Who Benefits? Central America, Coffee and the EU

Civil Society Organisations Demand Open and Ambitious Approval of CAP Plans

CAP Strategic Plans: Germany Taking Steps in the Right Direction?

CAP Strategic Plans: Support to High-Nature-Value Farming in Bulgaria

Commission’s Recommendations to CAP Strategic Plans: Glitters or Gold?

German Environment Ministry Proposals For CAP Green Architecture

CAP Performance Monitoring and Evaluation Framework – EP Position

A Rural Proofed CAP post 2020? – Analysis of the European Parliament’s Position

CAP Beyond the EU: The Case of Honduran Banana Supply Chains

CAP | Parliament’s Political Groups Make Moves as Committee System Breaks Down

CAP & the Global South: National Strategic Plans – a Step Backwards?

CAP Strategic Plans on Climate, Environment – Ever Decreasing Circles

European Green Deal | Revving Up For CAP Reform, Or More Hot Air?

Climate and environmentally ambitious CAP Strategic Plans: Based on what exactly?

How Transparent and Inclusive is the Design Process of the National CAP Strategic Plans?